Noticias de tecnología para el sector de la traducción

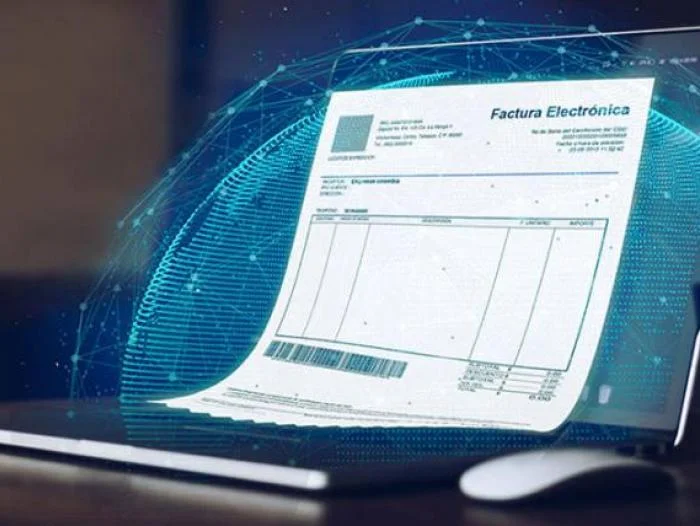

Factura electrónica obligatoria en España

Novedades marzo 2024

Hacemos un breve resumen de todo lo que necesitas saber (de momento)

Factura electrónica obligatoria en España

Novedades marzo 2024

Hacemos un breve resumen de todo lo que necesitas saber (de momento)